Use these links to rapidly review the document

TABLE OF CONTENTS

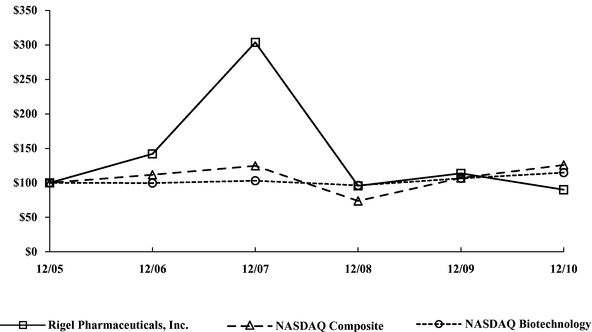

Item 8. Financial Statements and Supplementary Data

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| (Mark One) | ||

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended December 31, 2010 |

||

or |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

Commission file number 0-29889

RIGEL PHARMACEUTICALS, INC.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

94-3248524 (IRS Employer Identification No.) |

|

1180 Veterans Blvd. South San Francisco, California (Address of principal executive offices) |

94080 (Zip Code) |

(650) 624-1100

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class: | Name of each exchange on which registered: | |

|---|---|---|

| Common Stock, par value $.001 per share | The Nasdaq Global Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by a check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act).

| Large accelerated filer o | Accelerated filer ý | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by a check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

The approximate aggregate market value of the Common Stock held by non-affiliates of the registrant, based upon the closing price of the registrant's Common Stock as reported on the Nasdaq Global Market on June 30, 2010, the last business day of the registrant's most recently completed second fiscal quarter, was $372,591,482. Shares of the registrant's outstanding Common Stock held by each executive officer, director and affiliates of the registrant's outstanding Common Stock have been excluded. The determination of affiliate status for the purposes of this calculation is not necessarily a conclusive determination for other purposes.

As of February 23, 2011, there were 52,273,484 shares of the registrant's Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Items 10, 11, 12, 13 and 14 of Part III incorporate information by reference from the definitive proxy statement for the registrant's 2011 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission pursuant to Regulation 14A not later than 120 days after the end of the fiscal year covered by this Annual Report on Form 10-K.

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains statements indicating expectations about future performance and other forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the Exchange Act), that involve risks and uncertainties. We usually use words such as "may," "will," "should," "could," "expect," "plan," "anticipate," "believe," "estimate," "predict," "intend" or the negative of these terms or similar expressions to identify these forward-looking statements. These statements appear throughout this Annual Report on Form 10-K and are statements regarding our current intent, belief or expectation, primarily with respect to our operations and related industry developments. Examples of these statements include, but are not limited to, statements regarding the following: our business and scientific strategies; the progress of our product development programs, including clinical testing, and the timing of results thereof; our corporate collaborations, and revenues that may be received from collaborations; our drug discovery technologies; our research and development expenses; protection of our intellectual property; sufficiency of our cash resources; and our operations and legal risks. You should not place undue reliance on these forward-looking statements. Our actual results could differ materially from those anticipated in these forward-looking statements for many reasons, including as a result of the risks and uncertainties discussed under the heading "Risk Factors" in Part I, Item 1A of this Annual Report on Form 10-K. A forward-looking statement speaks only as of the date on which it is made, and we undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events. New factors emerge from time to time, and it is not possible for us to predict which factors will arise. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward- looking statements.

Overview

Rigel Pharmaceuticals, Inc. was incorporated in Delaware in June 1996, and is based in South San Francisco, California. We are a clinical-stage drug development company that discovers and develops novel, small-molecule drugs for the treatment of inflammatory and autoimmune diseases, as well as for muscle disorders. Our pioneering research focuses on intracellular signaling pathways and related targets that are critical to disease mechanisms. Our productivity has resulted in strategic collaborations with large pharmaceutical partners to develop and market our product candidates. Current product development programs include fostamatinib (previously referred to as R788), an oral syk inhibitor that has started its phase 3 clinical trial program for rheumatoid arthritis (RA) (partnered with AstraZeneca AB (AZ)), and R343, an inhaled syk inhibitor that is in clinical trials for asthma (partnered with Pfizer, Inc. (Pfizer)).

During 2010, we:

1

Strategy

Our research team is focused on creating a portfolio of product candidates that may be developed as small molecule therapeutics for our own proprietary programs and/or for development by potential collaborative partners. We recognize that the product development process is subject to both high costs and a high risk of failure. We believe that identifying a variety of product candidates and working in conjunction with other pharmaceutical partners may minimize the risk of failure, fill the product pipeline gap at major pharmaceutical companies and ultimately, increase the likelihood of advancing clinical development and potential commercialization of the product candidates.

The key elements to our scientific and business strategy are to:

Product Development Programs

Our product development portfolio features multiple novel, small-molecule drugs for the treatment of inflammatory and autoimmune diseases, as well as for muscle disorders.

Partnered Clinical Programs

Fostamatinib (previously referred to as R788)—Rheumatoid Arthritis

Disease background. RA is a systemic autoimmune inflammatory disease that causes damage to the joints and other organs, affecting approximately 1 in 100 people in the U.S. It is a major cause of disability and is also associated with reduced life expectancy, especially if it is not adequately treated. Despite current treatment options, many patients still experience significant disease activity, including continued joint destruction leading to pain and disability, so new treatment options are needed.

The current treatment options for RA have significant potential side effects and other shortfalls, including gastrointestinal complications and kidney damage. RA patients may receive multiple drugs depending on the extent and aggressiveness of their disease. Most RA patients eventually require some form of disease modifying anti-rheumatic drugs (DMARDs). This category of drugs includes methotrexate and a variety of intravenously-delivered immunomodulatory agents (anti-tumor necrosis factor (TNF) inhibitors and co-stimulation inhibitors).

Orally-available syk inhibitor program. Fostamatinib is an orally bio-available syk inhibitor. It has a novel mechanism of action for the treatment of RA in which it reversibly blocks signaling in multiple cell types involved in inflammation and tissue degradation (e.g., macrophages, osteoclasts, mast cells and B cells). RA is an autoimmune disease characterized by chronic inflammation that affects multiple tissues, but typically produces its most pronounced symptoms in the joints.

2

TASKi2

In July 2009, we announced that fostamatinib produced significant clinical improvement in RA patients in the TASKi2 Phase 2b clinical trial, which evaluated 457 RA patients for up to six months. TASKi2 was a multi-center, randomized, double-blind, placebo-controlled, parallel-dose clinical trial involving RA patients in the U.S., Latin America and Europe who had failed to respond to methotrexate alone. Patients received either 100 mg of fostamatinib b.i.d. (twice a day), 150 mg q.d. (once a day) or placebo.

Efficacy assessments for each participant were based on the American College of Rheumatology (ACR) criteria, which denotes at least 20% (ACR 20), at least 50% (ACR 50), or at least 70% (ACR 70) improvement, in addition to improvement denoted in the Disease Activity Score (DAS28), from each patient's baseline assessment at the end of the six month treatment period. The groups treated with 100 mg of fostamatinib b.i.d. and 150 mg q.d. reported higher response rates than the placebo group in all aforementioned criteria levels. The efficacy results for the two dosing groups were comparable, although the response rates for the 100 mg b.i.d. group were uniformly greater.

Consistent with the previous Phase 2a clinical trial (TASKi1), the onset effect of fostamatinib occurred within one week after the initiation of therapy and was maintained. The most frequent adverse events were expected based on results from TASKi1 and appeared to be manageable. The most common clinically meaningful drug-related adverse events noted in TASKi2 were diarrhea and hypertension. Dose reduction options were pre-specified in the trial protocol and, in cases where doses were reduced, patients generally completed the clinical trial with minimal safety issues. The mean increase in blood pressure at six months from baseline, using a last observation carry forward methodology, was less than 0.5 mmHg for the 150 mg q.d. dose group and approximately 1 mmHg for the 100 mg b.i.d. dose group. On the patients that had a history of high blood pressure, an elevated blood pressure level at screening or baseline, or were on blood pressure medication, approximately 29% in the 150 mg q.d. dose and 39% in the 100 mg b.i.d. dose groups, had blood pressure medication adjusted or initiated during the course of the study, compared with 12% of similar patients from the placebo group. On the patients that did not have a history of high blood pressure, were not on blood pressure medication or did not have an elevated blood pressure level at screening or baseline, approximately 4% from the 150 mg q.d. dose and 9% from the 100 mg b.i.d. dose groups had blood pressure medication initiated during the course of the study, compared with 3% of similar patients from the placebo group. For those patients who had their dose of blood pressure medications adjusted or initiated, their blood pressure was successfully reduced and was generally well controlled throughout the remainder of the trial. The blood pressure medications were standard doses of common blood pressure medication, such as angiotensin-converting enzyme (ACE) inhibitors or diuretics.

The most common adverse events in the trial overall were related to infections, though these were generally evenly distributed among the placebo and fostamatinib groups.

Data for TASKi2 was published in the New England Journal of Medicine in September 2010.

TASKi3

In July 2009, we also announced results for the TASKi3 Phase 2b clinical trial involving 219 RA patients who had failed to respond to at least one biologic treatment. In the TASKi3 clinical trial, patients received either 100 mg of fostamatinib b.i.d. or placebo b.i.d. for up to three months. The group treated with fostamatinib did not report significantly higher ACR 20, ACR 50, ACR 70 and DAS28 response rates than the placebo group at three months, and therefore, the trial failed to meet its efficacy endpoints. The objective components (C-Reactive Protein and Erythrocyte Sedimentation Rate) of these ACR scores did show a statistically significant difference; however, the subjective reported response rate components did not show a statistically significant difference as compared to placebo. Although the ACR scores for the fostamatinib group were within the expected range in this

3

patient population, the reported placebo response rates were considerably higher than seen in any other previous study of RA biologic failure patients and rose unaccountably between week six (at which point the reported response rates between fostamatinib and placebo were significantly different) and month three (when such reported response rates were no longer significantly different).

TASKi3 was the first clinical trial for fostamatinib in which anatomical changes in the patients' wrists and hands were evaluated using Magnetic Resonance Imaging and scored using the RAMRIS (Rheumatoid Arthritis Magnetic Resonance Imaging Scoring) system. Those results showed improvements in the treated group versus the placebo group in the Synovitis and Osteitis scores, while the Erosion scores, known to be the slowest to change, showed no significant effect at three months.

Similar to TASKi2, the most common clinically meaningful drug-related adverse events noted in TASKi3 were diarrhea and hypertension. Dose reduction options were pre-specified in the trial protocol and, in cases where doses were reduced, patients generally completed the clinical trial with minimal safety issues. The mean increase in blood pressure from baseline at three months, using a last observation carry forward methodology, was 3.2 - 3.6 mmHg for the fostamatinib group. In TASKi3, approximately 26% of the patients that had a history of high blood pressure, had an elevated blood pressure level at screening or baseline, or were on blood pressure medication, had their blood pressure medication adjusted or initiated during the course of the study, compared with 14% of similar patients in the placebo group. Approximately 5% of the patients with a history of high blood pressure, or who were not on blood pressure medication or did not have an elevated blood pressure level at screening or baseline, had their blood pressure medication initiated during the course of the study, compared with 3% of similar patients from the placebo group. For those patients who had dosages of blood pressure medications adjusted or initiated, their blood pressure was successfully reduced and was generally well controlled throughout the remainder of the trial. The blood pressure medications were standard doses of common blood pressure medications such as ACE inhibitors or diuretics.

The most common adverse events in the trial overall were related to infections, though these were generally evenly distributed among the placebo and fostamatinib groups.

OSKIRA

The OSKIRA (Oral Syk Inhibition in Rheumatoid Arthritis) Phase 3 clinical trial program is designed to investigate fostamatinib as a treatment for RA in patients with an inadequate response to DMARDs, including methotrexate (MTX). AZ announced that the OSKIRA clinical trial program will include three pivotal Phase 3 studies assessing the efficacy and tolerability of fostamatinib: two 12-month studies examining the effect of fostamatinib on patients responding inadequately to DMARDs (including MTX), and a six-month study assessing the effect of fostamatinib on patients who have previously responded inadequately to anti-TNF therapy. In September 2010, the first patient was enrolled in the OSKIRA clinical trial program. The OSKIRA clinical trial program also includes a fourth clinical trial, which is a six-month study for the evaluation of efficacy and safety of fostamatinib monotherapy in patients who are DMARD naïve, DMARD intolerant or have inadequate response to DMARDs. The fostamatinib clinical trial program is also expected to include long-term safety extension studies involving more than 2,000 of the patients recruited during the course of the Phase 2 and 3 clinical trial programs. The first anticipated filings of new drug applications with the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) based on the OSKIRA clinical trial program are planned for 2013.

Fostamatinib—Other Indications

In addition to RA, fostamatinib has been studied in patients with other immune disorders and some cancers. Our collaboration with AZ gives AZ sole responsibility for all development decisions for all indications except for one solid tumor oncology study, which was announced in June 2009 and is

4

funded, designed and implemented by the National Cancer Institute (NCI). Any decisions regarding this study are the responsibility of the NCI.

R343—Asthma

Disease background. Allergic asthma is a chronic inflammatory disorder of the airways. Asthma affects the lower respiratory tract and is marked by episodic flare-ups, or attacks, that can be life threatening. In some patients, allergens, such as pollen, trigger the production of immunoglobulin E (IgE) antibodies, which then bind to mast cells and cause an intracellular signal that results in the release of various chemical mediators. When this process occurs repeatedly over time, it creates persistent inflammation of the airway passages, resulting in the chronic congestion and airway obstruction associated with allergic rhinitis and asthma, respectively.

Inhaled syk inhibitor program. R343 is a potent syk inhibitor that blocks IgE receptor signaling. Mast cells play important roles in both early and late phase allergic reactions, and syk inhibitors could potentially prevent both phases.

In the first quarter of 2005, we announced a collaborative research and license agreement with Pfizer for the development of inhaled products for the treatment of allergic asthma and other respiratory diseases, such as chronic obstructive pulmonary disease. The collaboration was focused on our pre-clinical small molecule compounds, which inhibit syk. R343 is the oral syk inhibitor small molecule at the center of this collaboration. Pfizer has completed the Phase 1a clinical trial of an inhaled formulation of R343, which commenced in December 2007 and resulted in a milestone payment of $5.0 million to us. Pfizer completed an initial Phase 1b allergen challenge clinical trial. Pfizer has informed us that they plan on conducting an additional allergen challenge trial in 2011.

Research/Preclinical Programs

We are conducting proprietary research in the broad disease areas of inflammation/immunology and muscle wasting/muscle endurance. Within each disease area, our researchers are investigating mechanisms of action as well as screening compounds against potential novel targets and optimizing those leads that appear to have the greatest potential.

In the area of inflammation /immunology, we have a lead candidate in our oral janus kinase 3 (Jak3) inhibitor program and expect to begin clinical studies by the end of 2011. This program is focused on the treatment of transplant rejection, but could also extend to indications including RA and psoriasis. We also have a lead candidate in our ophthalmological Jak3 program and expect to begin clinical studies for this program in 2011. This program is expected to focus on Sjögren's disease (keratoconjunctivitis sicca, or KS). Additionally, we expect to select a compound for preclinical development in 2011 from our protein kinase C theta (PKCQ) inhibitor program, initially focusing on multiple sclerosis.

In the area of muscle atrophy and muscle endurance, we are focusing on several signaling pathways that are important for muscle homeostasis. We have developed a series of orally bioavailable compounds that activate AMP-activate protein kinase (AMPK), a critical enzyme that regulates metabolic/energy pathways in cells. Activation of AMPK has been shown to improve measurements of muscle endurance in animal models, and our molecules have demonstrated efficacy in animal models of endurance as well as diabetes. Our ongoing efforts are to determine structure/activity relationships of compounds and examine their experimental physiology. We expect to enter the clinic with this program in late 2012 or 2013 for the potential treatment of patients with congestive heart failure or chronic obstructive pulmonary disease who exhibit exercise intolerance.

We also have an active small molecule discovery program in muscle wasting. Muscle atrophy, or the loss of muscle mass, is associated with several disease states. Excessive loss of muscle in the context

5

of illness can contribute significantly to both morbidity and mortality rates. Many conditions that have associated muscle loss, including cancer, chronic heart failure, chronic kidney disease, mechanical ventilation and aging (sarcopenia), have significant patient populations that may benefit from therapeutics that counter such muscle loss. One of our core programs in this area is focused on myostatin signaling. Myostatin is a cytokine that signals via the type II activin receptors (ACVR2A and ACVR2B) and has been shown to inhibit muscle growth. We are currently performing structure activity relationship studies on several promising molecules from initial ACVR2A/2B screens, and are developing new screens and models for this program. We expect to enter the clinic with this program in the late 2012 or 2013 for the potential indication of ventilator associated disuse atrophy.

Corporate Collaborations

We conduct research and development programs independently and in conjunction with our corporate collaborators. We currently have the following active collaborations with three major pharmaceutical/biotechnology companies: AZ, relating to the use of fostamatinib for the treatment of RA and other indications; Pfizer, relating to the use of R343 intrapulmonary (inhaled) asthma and allergy therapeutics; and Daiichi Sankyo Co., Ltd., in the field of oncology. None of these collaborations currently provide us with regular research reimbursement. In each of these collaborations, if certain conditions are met, we are entitled to receive future milestone payments and royalties. We cannot guarantee that these conditions will be met, or that research and development efforts will be successful. As a result, we may not receive any further milestone payments or royalties under these agreements.

AstraZeneca

In February 2010, we entered into an exclusive worldwide license agreement with AZ for the development and commercialization of our oral syk inhibitors for the treatment of human diseases other than those primarily involving respiratory or pulmonary dysfunction. The agreement includes a license of rights to fostamatinib, previously known as R788, our late-stage investigational product candidate for the treatment of RA and other indications. AZ is responsible for conducting and funding all future development, regulatory filings, manufacturing and global commercialization of products containing most of our oral syk inhibitors. The agreement became effective on March 26, 2010 and we received an upfront payment from AZ of $100.0 million in April 2010.

Under the licensing agreement, our deliverables were: (i) granting a license of rights to fostamatinib, (ii) transfer of technology (know-how) related to fostamatinib, and (iii) conducting, at our expense, the fostamatinib open label extension study until it was transferred to AZ on September 25, 2010. We concluded that these deliverables should be accounted for as one single unit of accounting and we recognized the $100.0 million upfront payment received in April 2010 from AZ ratably over the performance period from March 26, 2010, the effective date of the agreement, through September 25, 2010, the completion date of the last deliverable, which was the transfer of the fostamatinib long-term open label extension study to AZ. We elected a straight-line method for recognition of this upfront payment as the effort to advance and transfer the study was fairly consistent over the transition period.

On September 29, 2010, we announced that we earned $25.0 million from AZ in consideration for the fulfillment of two major milestones in the agreement. The first milestone was the initiation of the Phase 3 clinical trial program with fostamatinib in patients with RA that was announced by AZ on September 29, 2010. The second milestone was the completion of the transfer of the fostamatinib long-term open label extension study to AZ, which was also completed in September 2010. AZ is required to pay us up to an additional $320.0 million if specified development, regulatory and launch milestones are achieved for fostamatinib. We are also eligible to receive up to an additional $800.0 million if specified sales performance milestones are achieved for fostamatinib, as well as significant stepped double-digit royalties on net worldwide sales, if any.

6

Either party may terminate the agreement if the other party materially breaches the agreement and such breach remains uncured within 60 days from the date of notice, or in the event of insolvency of the other party. We may also terminate the agreement in its entirety if AZ challenges the validity, enforceability or scope of any of our patents licensed to AZ by us under the agreement. AZ may also terminate the agreement either without cause upon 180 days' written notice, or in the event of any change of control of Rigel upon 30 days' written notice. If neither party terminates the agreement, then the agreement will remain in effect until the cessation of all commercial sales of all products subject to the agreement, including fostamatinib.

Pfizer

In January 2005, we entered into a research collaboration with Pfizer that has a license component. The collaboration is for the development of inhaled products for the treatment of allergic asthma and other respiratory diseases such as chronic obstructive pulmonary disease. The collaboration was primarily focused on our preclinical small molecule compounds, which inhibit IgE receptor signaling in respiratory tract mast cells by blocking the signaling enzyme syk. A goal of the collaboration was for Pfizer to nominate a licensed compound to commence advanced preclinical development. Pfizer is responsible for the manufacture of all preclinical and clinical materials for each compound/product and all costs associated with development and commercialization. We did not have any further obligations to Pfizer after the research phase of the collaboration ended in February 2007.

In connection with this collaboration, Pfizer paid us upfront fees of $10.0 million and purchased $5.0 million of our common stock at a premium in 2005. We have earned and will continue to earn milestone payments in connection with certain clinical events, should they occur, as well as royalties from sales of the resulting products upon marketing approval, if any. Under the terms of the collaboration agreement, the aggregate of potential milestone amounts payable to us is $175.0 million and mid-single-digit to low double-digit royalties on sales. In May 2006, we achieved the first milestone upon selection of the licensed compound and received a $5.0 million milestone payment when Pfizer nominated R343 to commence advanced preclinical development in allergic asthma. In December 2007, we received a second milestone payment of $5.0 million when Pfizer initiated a Phase 1 clinical trial on R343. No milestone payments were received in 2008, 2009 and 2010 as no further milestones were achieved. Pfizer completed an initial Phase 1b allergen challenge clinical trial. Pfizer has informed us that they plan on conducting an additional allergen challenge trial in 2011. Pfizer remains obligated to pay us various milestones and royalties in the future if certain conditions are achieved.

Pfizer may terminate the collaboration agreement for any reason upon prior written notice to us, for cause if we materially breach the agreement and such breach remains uncured, or if we become insolvent. We may terminate the collaboration agreement for cause if Pfizer fails to meet certain diligence efforts, materially breaches the agreement and such breach remains uncured, or becomes insolvent. If neither party exercises its option to terminate the collaboration agreement, then the agreement automatically terminates on the later of: (1) the last valid claim to expire covering a licensed product and (2) after a specified period from the launch of a licensed product.

Daiichi Sankyo

In August 2002, we signed an agreement for a collaboration with Daiichi Sankyo (Daiichi) to pursue research related to a specific target from a novel class of drug targets called ligases that control cancer cell proliferation through protein degradation. Daiichi paid us $0.9 million at the time we entered into the agreement. Under the terms of the collaboration agreement, the aggregate of potential milestone amounts payable to us is $33.9 million and we are entitled to receive royalties on any commercialized products to emerge from the collaboration at low to mid-single-digit royalties on sales. We have earned to date milestone payments totaling $5.7 million, including a milestone payment of $750,000 for the first designation of a rational design lead compound that we received in December

7

2009, and may earn additional milestone payments in connection with certain clinical events. The research phase of this three-year collaboration expired in August 2005. Under the terms of the agreement, we retain the rights to co-develop and co-promote certain products resulting from this collaboration in North America, while Daiichi retains co-development and promotion rights in the remainder of the world.

Either party may terminate the collaboration agreement if the other party materially breaches the agreement and such breach remains uncured, or after a specified period from the end of a designated research period if no product is commercialized (unless the parties agree to extend the collaboration). The collaboration agreement can also be terminated by mutual written consent of the parties. If neither party exercises its option to terminate the collaboration agreement, then the agreement automatically terminates on the later of (1) the expiration of the last patent with a claim that covers the composition of matter of a product (or manufacture or use of a product under certain circumstances) and (2) after a specified period from the initial commercialization of a licensed product.

Our Discovery Engine

The technologies that we use in connection with both our proprietary product development programs and our corporate collaborations are designed to identify protein targets for compound screening and validate the role of those targets in the disease process. Unlike genomics-based approaches, which begin by identifying genes and then searching for their functions, our approach identifies proteins that are demonstrated to have an important role in a specific disease pathway. By understanding the disease pathway, we attempt to avoid studying genes that will not make good drug targets and focus only on the subset of expressed proteins of genes that we believe are specifically implicated in the disease process.

We begin by developing assays that model the key events in a disease process at the cellular level. We then search hundreds of millions of cells to identify potential protein targets. In addition, we identify the proteins involved in the intracellular process and prepare a map of their interactions, thus giving us a comprehensive picture of the intracellular disease pathway. We believe that our approach has a number of advantages, including:

Because of the very large number of cells and proteins employed, our technology is labor intensive. The complexity of our technology requires a high degree of skill and diligence to perform successfully.

8

In addition, successful application of our technology depends on a highly diverse collection of proteins to test in cells. We believe we have been and will continue to be able to meet these challenges successfully and increase our ability to identify targets for drug discovery. Although other companies may utilize technologies similar to certain aspects of our technology, we are unaware of any other company that employs the same combination of technologies that we do.

Pharmacology and Preclinical Development

We believe that the rapid characterization and optimization of lead compounds identified in high throughput screening (HTS) will generate high quality preclinical development candidates. Our pharmacology and preclinical development group facilitates lead optimization by characterizing lead compounds with respect to pharmacokinetics, potency, efficacy and selectivity. The generation of proof-of-principle data in animals and the establishment of standard pharmacological models with which to assess lead compounds represent integral components of lead optimization. As programs move through the lead optimization stage, our pharmacology and preclinical development groups support our chemists and biologists by performing the necessary studies, including toxicology, for investigational new drug (IND) application submissions.

Clinical Development

We have assembled a team of experts in drug development to design and implement clinical trials and to analyze the data derived from these trials. The clinical development group possesses expertise in project management and regulatory affairs.

Intellectual Property

We are able to protect our technology from unauthorized use by third parties only to the extent that it is covered by valid and enforceable patents or is effectively maintained as a trade secret. Accordingly, patents and other proprietary rights are an essential element of our business. We have over 95 pending patent applications and over 185 issued patents in the United States, as well as pending corresponding foreign patent applications and issued foreign patents. Our policy is to file patent applications to protect technology, inventions and improvements to inventions that are commercially important to the development of our business. We seek United States and international patent protection for a variety of technologies, including new screening methodologies and other research tools, target molecules that are associated with disease states identified in our screens, and lead compounds that can affect disease pathways. We also intend to seek patent protection or rely upon trade secret rights to protect other technologies that may be used to discover and validate targets and that may be used to identify and develop novel drugs. We seek protection, in part, through confidentiality and proprietary information agreements. We are a party to various license agreements that give us rights to use technologies in our research and development.

Our patents extend for varying periods according to the date of patent filing or grant and the legal term of patents in the various countries where patent protection is obtained. Our material patents relate to compositions of matter covering specific drug candidates in clinical trials that target syk. These patents will expire, excluding patent term adjustments and extensions, in 2023, 2024 and 2026. Several of these patents will have patent term adjustments and extensions depending on the length of time required to conduct clinical trials.

We currently hold a number of issued patents in the United States, as well as corresponding applications that allow us to pursue patents in other countries, some of which have been allowed and/or granted and others of which we expect to be granted. Specifically, in most cases where we hold a U.S. issued patent, the subject matter is covered at least by an application filed under the Patent Cooperation Treaty (PCT), which is then used or has been used to pursue protection in certain

9

countries that are members of the treaty. Our material patents relate to fostamatinib, an oral syk inhibitor, and R406, the active metabolite of fostamatinib.

Fostamatinib. Fostamatinib is covered as a composition of matter in a U.S. issued patent that has an expiration date in September 2026, after taking into account a patent term adjustment, and may be granted further protection under the patent term extension rules related to conducting clinical trials. Fostamatinib is also covered under broader composition of matter claims in a U.S. issued patent that has an expiration date in March 2026, after taking into account a patent term adjustment. Methods of using fostamatinib to treat various indications, methods of making fostamatinib, and compositions of matter covering certain intermediates used to make fostamatinib are also covered, respectively, in three U.S. issued patents; the earliest expiration date of any of these patents is in April 2023 and the latest expiration date is in June 2026, after taking into account patent term adjustments. Corresponding applications have been filed in foreign jurisdictions under the PCT, and are at various stages of prosecution. Of note, a patent covering fostamatinib as a composition of matter and in compositions for use treating various diseases has been granted by the European Patent Office.

R406. R406 is covered as a composition of matter in a U.S. issued patent and, with a patent term adjustment, currently has an expiration date in February 2025. R406 is also covered under two broader composition of matter patents issued in the U.S. expiring in February 2023 and July 2024. Methods of using R406 to treat various indications and compositions of matter covering certain intermediates used to make R406 are also covered under patents described above. Corresponding applications have been filed in foreign jurisdictions under the PCT, and are at various stages of prosecution.

Competition

The biotechnology and pharmaceutical industries are intensely competitive and subject to rapid and significant technological change. Many of the drugs that we are attempting to discover will be competing with existing therapies. In addition, a number of companies are pursuing the development of pharmaceuticals that target the same diseases and conditions that we are targeting. We face, and will continue to face, intense competition from pharmaceutical and biotechnology companies, as well as from academic and research institutions and government agencies, both in the United States and abroad. Some of these competitors are pursuing the development of pharmaceuticals that target the same diseases and conditions as our research programs. Our major competitors include fully integrated pharmaceutical companies that have extensive drug discovery efforts and are developing novel small molecule pharmaceuticals. We also face significant competition from organizations that are pursuing the same or similar technologies, including the discovery of targets that are useful in compound screening, as the technologies used by us in our drug discovery efforts.

Competition may also arise from:

Our competitors or their collaborative partners may utilize discovery technologies and techniques or partner with collaborators in order to develop products more rapidly or successfully than we or our collaborators are able to do. Many of our competitors, particularly large pharmaceutical companies, have substantially greater financial, technical and human resources and larger research and development staffs than we do. In addition, academic institutions, government agencies and other public and private organizations conducting research may seek patent protection with respect to

10

potentially competitive products or technologies and may establish exclusive collaborative or licensing relationships with our competitors.

We believe that our ability to compete is dependent, in part, upon our ability to create, maintain and license scientifically-advanced technology and upon our and our collaborators' ability to develop and commercialize pharmaceutical products based on this technology, as well as our ability to attract and retain qualified personnel, obtain patent protection or otherwise develop proprietary technology or processes and secure sufficient capital resources for the expected substantial time period between technological conception and commercial sales of products based upon our technology. The failure by any of our collaborators or us in any of those areas may prevent the successful commercialization of our potential drug targets.

Many of our competitors, either alone or together with their collaborative partners, have significantly greater experience than we do in:

Accordingly, our competitors may succeed in obtaining patent protection, identifying or validating new targets or discovering new drug compounds before we do.

Our competitors might develop technologies and drugs that are more effective or less costly than any that are being developed by us or that would render our technology and product candidates obsolete and noncompetitive. In addition, our competitors may succeed in obtaining the approval of the FDA or other regulatory agencies for product candidates more rapidly. Companies that complete clinical trials, obtain required regulatory agency approvals and commence commercial sale of their drugs before their competitors may achieve a significant competitive advantage, including certain patent and FDA marketing exclusivity rights that would delay or prevent our ability to market certain products. Any drugs resulting from our research and development efforts, or from our joint efforts with our existing or future collaborative partners, might not be able to compete successfully with competitors' existing or future products or obtain regulatory approval in the United States or elsewhere.

We face and will continue to face intense competition from other companies for collaborative arrangements with pharmaceutical and biotechnology companies, for establishing relationships with academic and research institutions and for licenses to additional technologies. These competitors, either alone or with their collaborative partners, may succeed in developing technologies or products that are more effective than ours.

Our ability to compete successfully will depend, in part, on our ability to:

11

Research and Development Expenses

A significant portion of our operating expenses is related to research and development and we intend to maintain our strong commitment to research and development. See "Item 8. Financial Statements and Supplementary Data" of this Annual Report on Form 10-K for costs and expenses related to research and development, and other financial information for fiscal years 2010, 2009, and 2008.

Government Regulation

Our ongoing development activities are and will continue to be subject to extensive regulation by numerous governmental authorities in the United States and other countries, including the FDA, under the Federal Food, Drug and Cosmetic Act. The regulatory review and approval process is expensive and uncertain. Securing FDA approval requires the submission of extensive preclinical and clinical data and supporting information to the FDA for each indication to establish a product candidate's safety and efficacy.

Preclinical studies generally are conducted in laboratory animals to evaluate the potential safety and the efficacy of a product. Drug developers submit the results of preclinical studies to the FDA as part of an IND application that must be approved before clinical trials can begin in humans. Typically, clinical evaluation involves a time consuming and costly three-phase process.

The approval process takes many years, requires the expenditure of substantial resources and may involve ongoing requirements for post-marketing studies. Clinical trials are subject to oversight by institutional review boards and the FDA. In addition, clinical trials:

Even if we are able to achieve success in our clinical testing, we, or our collaborative partners, must provide the FDA and foreign regulatory authorities with clinical data that demonstrates the safety and efficacy of our products in humans before they can be approved for commercial sale. We do not know whether any future clinical trials will demonstrate sufficient safety and efficacy necessary to obtain the requisite regulatory approvals or will result in marketable products. Our failure, or the failure of our strategic partners, to adequately demonstrate the safety and efficacy of our products under development will prevent receipt of FDA and similar foreign regulatory approval and, ultimately, commercialization of our products.

12

Any clinical trial may fail to produce results satisfactory to the FDA. Preclinical and clinical data can be interpreted in different ways, which could delay, limit or prevent regulatory approval. Negative or inconclusive results or adverse medical events during a clinical trial could cause a clinical trial to be repeated or a program to be terminated. In addition, delays or rejections may be encountered based upon additional government regulation from future legislation or administrative action or changes in FDA policy or interpretation during the period of product development, clinical trials and FDA regulatory review. Failure to comply with applicable FDA or other applicable regulatory requirements may result in criminal prosecution, civil penalties, recall or seizure of products, total or partial suspension of production or injunction, as well as other regulatory action against our potential products, collaborative partners or us.

Outside the United States, our ability to market a product is contingent upon receiving a marketing authorization from the appropriate regulatory authorities. The requirements governing the conduct of clinical trials, marketing authorization, pricing and reimbursement vary widely from country to country. At present, foreign marketing authorizations are applied for at a national level, although within the European Union (EU), registration procedures are available to companies wishing to market a product in more than one EU member state. If the regulatory authority is satisfied that adequate evidence of safety, quality and efficacy has been presented, a marketing authorization will be granted. This foreign regulatory approval process involves all of the risks associated with FDA clearance.

Manufacturing and Raw Materials

We currently rely on, and will continue to rely on, third party contract manufacturers to produce sufficient quantities of our product candidates for use in our preclinical and anticipated clinical trials.

Employees

As of December 31, 2010, we had 145 employees. None of our employees are represented by a collective bargaining arrangement, and we believe our relationship with our employees is good. Recruiting and retaining qualified scientific personnel to perform research and development work in the future will be critical to our success. We may not be able to attract and retain personnel on acceptable terms given the competition among pharmaceutical and biotechnology companies, academic and research institutions and government agencies for experienced scientists.

Scientific and Medical Advisors

We utilize scientists and physicians to advise us on scientific and medical matters as part of our ongoing research and product development efforts, including experts in clinical trial design, preclinical development work, chemistry, biology, infectious diseases, immunology and oncology. Certain of our scientific and medical advisors and consultants receive an option to purchase our common stock and an honorarium for time spent assisting us.

Available Information

Our website is located at www.rigel.com. The information found on our website is not incorporated by reference into this Annual Report on Form 10-K. We electronically file with the Securities and Exchange Commission (SEC) our Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, our director and officers' Section 16 reports and other SEC filings and amendments to the reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act. We make available free of charge on or through our website copies of these reports as soon as reasonably practicable after we electronically file these reports with, or furnish them to, the SEC. Further, a copy of these reports is located at the SEC's Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. Information on the operation of the Public Reference Room can be obtained

13

by calling the SEC at 1-800-SEC-0330. The SEC also maintains an internet site that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC at www.sec.gov.

In evaluating our business, you should carefully consider the following risks, as well as the other information contained in this Annual Report on Form 10-K. These risk factors could cause our actual results to differ materially from those contained in forward-looking statements we have made in this Annual Report on Form 10-K and those we may make from time to time. If any of the following risks actually occurs, our business, financial condition and operating results could be harmed. The risks and uncertainties described below are not the only ones facing us. Additional risks and uncertainties not presently known to us, or that we currently see as immaterial, may also harm our business.

If our corporate collaborations or license agreements are unsuccessful, our research and development efforts could be delayed.

Our strategy depends upon the formation and sustainability of multiple collaborative arrangements and license agreements with third parties now and in the future. We rely on these arrangements for not only financial resources, but also for expertise we need now and in the future relating to clinical trials, manufacturing, sales and marketing, and for licenses to technology rights. To date, we have entered into several such arrangements with corporate collaborators; however, we do not know if these collaborations or additional third parties with which we may collaborate, if any, will dedicate sufficient resources or if any development or commercialization efforts by third parties will be successful. In addition, our corporate collaborators may delay clinical trials, provide insufficient funding for a clinical trial program, stop a clinical trial or abandon a drug candidate. Although Pfizer has informed us that they plan to conduct an allergen challenge trial in 2011, they may later decide to delay or discontinue the trial. Should a collaborative partner fail to develop or commercialize a compound or product to which it has rights from us for any reason, including corporate restructuring, such failure might delay our ongoing research and development efforts, because we might not receive any future milestone payments, and we would not receive any royalties associated with such compound or product. In addition, the continuation of some of our partnered drug discovery and development programs may be dependent on the periodic renewal of our corporate collaborations.

In February 2010, we entered into an exclusive worldwide license agreement with AZ for the global development and commercialization of our oral syk inhibitors for the treatment of human diseases other than those primarily involving respiratory or pulmonary dysfunction. The agreement includes a license of rights to fostamatinib, our late-stage investigational product candidate for the treatment of RA and other indications. AZ started its Phase 3 clinical trial program in patients in RA in September 2010. Our collaboration agreement with AZ does not include a research phase. The research phase of our collaboration with Johnson & Johnson ended in 2003, and the research phases conducted at our facilities under our broad collaboration with Novartis Pharma AG (Novartis) ended in 2004. The research phase of our collaboration agreement with Daiichi ended in 2005. In 2004, we signed a new collaboration agreement with Merck & Co., Inc. (Merck), and the research phase of this collaboration ended in May 2007. In 2005, we signed a new collaboration agreement with Pfizer, and the research phase of this collaboration ended in February 2007. Our collaboration agreement with Merck Serono, which, as of February 2010, is no longer active, did not include a research phase. Each of our collaborations could be terminated by the other party at any time, and we may not be able to renew these collaborations on acceptable terms, if at all, or negotiate additional corporate collaborations on acceptable terms, if at all. If these collaborations terminate or are not renewed, any resultant loss of revenues from these collaborations or loss of the resources and expertise of our collaborative partners could adversely affect our business.

14

Conflicts also might arise with collaborative partners concerning proprietary rights to particular compounds. While our existing collaborative agreements typically provide that we retain milestone payments and royalty rights with respect to drugs developed from certain derivative compounds, any such payments or royalty rights may be at reduced rates, and disputes may arise over the application of derivative payment provisions to such drugs, and we may not be successful in such disputes.

We are also a party to various license agreements that give us rights to use specified technologies in our research and development processes. The agreements pursuant to which we have in-licensed technology permit our licensors to terminate the agreements under certain circumstances. If we are not able to continue to license these and future technologies on commercially reasonable terms, our product development and research may be delayed or otherwise adversely affected.

If conflicts arise between our collaborators or advisors and us, any of them may act in their self-interest, which may be adverse to our stockholders' interests.

If conflicts arise between us and our corporate collaborators or scientific advisors, the other party may act in its self-interest and not in the interest of our stockholders. Some of our corporate collaborators are conducting multiple product development efforts within each disease area that is the subject of the collaboration with us or may be acquired or merged with a company having a competing program. In some of our collaborations, we have agreed not to conduct, independently or with any third party, any research that is competitive with the research conducted under our collaborations. Our collaborators, however, may develop, either alone or with others, products in related fields that are competitive with the products or potential products that are the subject of these collaborations. Competing products, either developed by our collaborators or to which our collaborators have rights, may result in their withdrawal of support for our product candidates.

If any of our corporate collaborators were to breach or terminate its agreement with us or otherwise fail to conduct the collaborative activities successfully and in a timely manner, the preclinical or clinical development or commercialization of the affected product candidates or research programs could be delayed or terminated. We generally do not control the amount and timing of resources that our corporate collaborators devote to our programs or potential products. We do not know whether current or future collaborative partners, if any, might pursue alternative technologies or develop alternative products either on their own or in collaboration with others, including our competitors, as a means for developing treatments for the diseases targeted by collaborative arrangements with us.

If we are unable to obtain regulatory approval to market products in the United States and foreign jurisdictions, we will not be permitted to commercialize products from our research and development.

We cannot predict whether regulatory clearance will be obtained for any product that we, or our collaborative partners, hope to develop. Satisfaction of regulatory requirements typically takes many years, is dependent upon the type, complexity and novelty of the product and requires the expenditure of substantial resources. Of particular significance to us are the requirements relating to research and development and testing.

Before commencing clinical trials in humans in the United States, we, or our collaborative partners, will need to submit and receive approval from the FDA of an IND. Clinical trials are subject to oversight by institutional review boards and the FDA and:

15

While we have stated that we intend to file additional INDs, this is only a statement of intent, and we may not be able to do so because we may not be able to identify potential product candidates. In addition, the FDA may not approve any IND in a timely manner, or at all.

Before receiving FDA approval to market a product, we must demonstrate with substantial clinical evidence that the product is safe and effective in the patient population and the indication that will be treated. Data obtained from preclinical and clinical activities are susceptible to varying interpretations that could delay, limit or prevent regulatory approvals. In addition, delays or rejections may be encountered based upon additional government regulation from future legislation or administrative action or changes in FDA policy during the period of product development, clinical trials and FDA regulatory review. Failure to comply with applicable FDA or other applicable regulatory requirements may result in criminal prosecution, civil penalties, recall or seizure of products, total or partial suspension of production or injunction, adverse publicity, as well as other regulatory action against our potential products or us. Additionally, we have limited experience in conducting and managing the clinical trials necessary to obtain regulatory approval.

If regulatory approval of a product is granted, this approval will be limited to those indications or disease states and conditions for which the product is demonstrated through clinical trials to be safe and efficacious. We cannot ensure that any compound developed by us, alone or with others, will prove to be safe and efficacious in clinical trials and will meet all of the applicable regulatory requirements needed to receive marketing approval.

Outside the United States, our ability, or that of our collaborative partners, to market a product is contingent upon receiving a marketing authorization from the appropriate regulatory authorities. This foreign regulatory approval process typically includes all of the risks and costs associated with FDA approval described above and may also include additional risks and costs.

We might not be able to commercialize our product candidates successfully if problems arise in the clinical testing and approval process.

Commercialization of our product candidates depends upon successful completion of extensive preclinical studies and clinical trials to demonstrate their safety and efficacy for humans. Preclinical testing and clinical development are long, expensive and uncertain processes.

In connection with clinical trials of our product candidates, we face the risks that:

16

We do not know whether we, or any of our collaborative partners, will be permitted to undertake clinical trials of potential products beyond the trials already concluded and the trials currently in process. It will take us, or our collaborative partners several years to complete any such testing, and failure can occur at any stage of testing. Interim results of trials do not necessarily predict final results, and acceptable results in early trials may not be repeated in later trials. A number of companies in the pharmaceutical industry, including biotechnology companies, have suffered significant setbacks in advanced clinical trials, even after achieving promising results in earlier trials. Moreover, we or our collaborative partners or regulators may decide to discontinue development of any or all of these projects at any time for commercial, scientific or other reasons.

There is a high risk that drug discovery and development efforts might not successfully generate good product candidates.

At the present time, the majority of our operations are in various stages of drug identification and development. We currently have two product compounds in the clinical testing stage: one with indications for RA, as well as for certain solid tumors that is being implemented by the NCI, all of which indications are subject to a collaboration agreement with AZ; and one in Phase 1b testing and intended for allergic asthma, which is subject to a collaboration agreement with Pfizer. In our industry, it is statistically unlikely that the limited number of compounds that we have identified as potential product candidates will actually lead to successful product development efforts, and we do not expect any drugs resulting from our research to be commercially available for several years, if at all.

Our compounds in clinical trials and our future leads for potential drug compounds are subject to the risks and failures inherent in the development of pharmaceutical products. These risks include, but are not limited to, the inherent difficulty in selecting the right drug and drug target and avoiding unwanted side effects, as well as unanticipated problems relating to product development, testing, obtaining regulatory approvals, maintaining regulatory compliance, manufacturing, competition and costs and expenses that may exceed current estimates. For example, in our two Phase 2b clinical trials for fostamatinib in RA, TASKi2 and TASKi3, the most common clinically meaningful drug-related adverse events noted were diarrhea and hypertension. In both our TASKi2 and TASKi3 Phase 2b clinical trials, a meaningfully higher percentage of patients in the fostamatinib treatment groups had blood pressure medication adjusted or initiated during the course of the clinical trials as compared to the placebo group. In larger future clinical trials, we may discover additional side effects and/or higher frequency of side effects than those observed in completed clinical trials. If approved by the FDA, the side effect profile of fostamatinib may also result in a narrowly approved indication for use of the product, especially in light of other drugs currently available to treat RA, dependent on the safety profile of fostamatinib relative to those drugs.

The results of preliminary and mid-stage studies do not necessarily predict clinical or commercial success, and larger later-stage clinical trials may fail to confirm the results observed in the previous studies. Similarly, a clinical trial may show that a product candidate is safe and effective for certain patient populations in a particular indication, but other clinical trials may fail to confirm those results in a subset of that population or in a different patient population, which may limit the potential market for that product candidate. For example, fostamatinib produced significant clinical improvement in RA patients who had failed to respond to methotrexate alone in our TASKi2 Phase 2b clinical trial, but our TASKi3 Phase 2b clinical trial failed to meet its efficacy endpoints in RA patients who had failed to respond to at least one biologic treatment. In addition, if we were to repeat either of the TASKi2 and TASKi3 Phase 2b clinical trials, any such additional trials may not confirm the results observed in the original trials. The Phase 3 clinical program evaluating fostamatinib in RA patients, initiated by our partner, AZ, may not show fostamatinib to be safe and effective for the treatment of RA patients. Finally, with respect to our own compounds in development, we have established anticipated timelines

17

with respect to the initiation of clinical studies based on existing knowledge of the compound. However, we cannot provide assurance that we will meet any of these timelines for clinical development.

Because of the uncertainty of whether the accumulated preclinical evidence (pharmacokinetic, pharmacodynamic, safety and/or other factors) or early clinical results will be observed in later clinical trials, we can make no assurances regarding the likely results from our future clinical trials or the impact of those results on our business.

Our success is dependent on intellectual property rights held by us and third parties, and our interest in such rights is complex and uncertain.

Our success will depend to a large part on our own, our licensees' and our licensors' ability to obtain and defend patents for each party's respective technologies and the compounds and other products, if any, resulting from the application of such technologies. We have over 95 pending patent applications and over 185 issued patents in the United States, as well as pending corresponding foreign patent applications and issued foreign patents. In the future, our patent position might be highly uncertain and involve complex legal and factual questions. For example, we may be involved in interferences before the United States Patent and Trademark Office. Interferences are complex and expensive legal proceedings and there is no assurance we will be successful in any such proceedings. An interference could result in our losing our patent rights and/or our freedom to operate and/or require us to pay significant royalties. Additional uncertainty may result because no consistent policy regarding the breadth of legal claims allowed in biotechnology patents has emerged to date. Accordingly, we cannot predict the breadth of claims allowed in our or other companies' patents.

Because the degree of future protection for our proprietary rights is uncertain, we cannot ensure that:

We rely on trade secrets to protect technology where we believe patent protection is not appropriate or obtainable; however, trade secrets are difficult to protect. While we require employees, collaborators and consultants to enter into confidentiality agreements, we may not be able to adequately protect our trade secrets or other proprietary information in the event of any unauthorized use or disclosure or the lawful development by others of such information.

We are a party to certain in-license agreements that are important to our business, and we generally do not control the prosecution of in-licensed technology. Accordingly, we are unable to exercise the same degree of control over this intellectual property as we exercise over our internally-developed technology. Moreover, some of our academic institution licensors, research collaborators and scientific advisors have rights to publish data and information in which we have rights. If we cannot maintain the confidentiality of our technology and other confidential information in connection with our collaborations, our ability to receive patent protection or protect our proprietary information may

18

otherwise be impaired. In addition, some of the technology we have licensed relies on patented inventions developed using U.S. government resources. The U.S. government retains certain rights, as defined by law, in such patents, and may choose to exercise such rights. Certain of our in-licenses may be terminated if we fail to meet specified obligations. If we fail to meet such obligations and any of our licensors exercise their termination rights, we could lose our rights under those agreements. If we lose any of our rights, it may adversely affect the way we conduct our business. In addition, because certain of our licenses are sublicenses, the actions of our licensors may affect our rights under those licenses.

If a dispute arises regarding the infringement or misappropriation of the proprietary rights of others, such dispute could be costly and result in delays in our research and development activities and partnering.

Our success will depend, in part, on our ability to operate without infringing or misappropriating the proprietary rights of others. There are many issued patents and patent applications filed by third parties relating to products or processes that are similar or identical to our licensors or ours, and others may be filed in the future. There can be no assurance that our activities, or those of our licensors, will not infringe patents owned by others. We believe that there may be significant litigation in the industry regarding patent and other intellectual property rights, and we do not know if our collaborators or we would be successful in any such litigation. Any legal action against our collaborators or us claiming damages or seeking to enjoin commercial activities relating to the affected products, our methods or processes could:

We will need additional capital in the future to sufficiently fund our operations and research.

We have consumed substantial amounts of capital to date as we continue our research and development activities, including preclinical studies and clinical trials. In February 2010, we entered into an exclusive worldwide license agreement with AZ for the global development and commercialization of our oral syk inhibitors for the treatment of human diseases other than those primarily involving respiratory or pulmonary dysfunction. The agreement includes a license of rights to fostamatinib, our late-stage investigational product candidate for the treatment of RA and other indications. The agreement became effective on March 26, 2010 and, in connection with the effectiveness of the agreement, we received an upfront payment of $100.0 million in April 2010 from AZ. In October 2010, we received $25.0 million from AZ in connection with the fulfillment of two major milestones in the agreement. The first milestone payment received was for initiation of the Phase 3 clinical program with fostamatinib in patients with RA that was announced by AZ in September 2010. The second milestone payment received was for the completion of the transfer of the fostamatinib long-term open label extension study to AZ. AZ is required to pay us up to an additional $320.0 million if specified development, regulatory and launch milestones are achieved for fostamatinib. We are also eligible to receive up to an additional $800.0 million if specified sales performance milestones are achieved for fostamatinib, as well as significant stepped double-digit royalties on net sales worldwide. We believe that our existing capital resources and the anticipated proceeds from our current collaborations will be sufficient to support our current and projected funding requirements through at least the next 12 months. We may need additional funds in the future and the amount of future funds needed will

19

depend largely on the success of our internally developed programs as they proceed in later and more expensive clinical trials. Unless and until we are able to generate a sufficient amount of product and royalty revenue, we expect to finance future cash needs through public and/or private offerings of equity securities, debt financings or collaboration and licensing arrangements, as well as through interest income earned on the investment of our cash balances and short-term investments. With the exception of milestone and royalty payments that we may receive under our existing collaborations, we do not currently have any commitments for future funding. We do not know whether additional financing will be available when needed, or that, if available, we will obtain financing on reasonable terms.

To the extent we raise additional capital by issuing equity securities, our stockholders could at that time experience substantial dilution. Any debt financing that we are able to obtain may involve operating covenants that restrict our business. To the extent that we raise additional funds through any new collaboration and licensing arrangements, we may be required to relinquish some rights to our technologies or product candidates, or grant licenses on terms that are not favorable to us.

Our future funding requirements will depend on many uncertain factors.

Our future funding requirements will depend upon many factors, including, but not limited to:

Insufficient funds may require us to delay, scale back or eliminate some or all of our research and development programs, to lose rights under existing licenses or to relinquish greater or all rights to product candidates at an earlier stage of development or on less favorable terms than we would otherwise choose or may adversely affect our ability to operate as a going concern.

Our success as a company is uncertain due to our history of operating losses and the uncertainty of future profitability.

Although we generated operating income of approximately $35.3 million for the year ended December 31, 2010, this resulted from the one-time upfront payment from AZ received in April 2010, as well as two milestone payments received from AZ in October 2010. We have historically operated at

20

a loss each year since we were incorporated in June 1996, due in large part to the significant research and development expenditures required to identify and validate new product candidates and pursue our development efforts. We expect to continue to incur net operating losses in the next three years and there can be no assurance that we will generate operating income in the future. For the years ended December 31, 2009 and 2008, we incurred net losses of approximately $111.5 million and $132.3 million, respectively. Currently, our only potential source of revenues is upfront payments, research and development milestone and royalty payments pursuant to our collaboration arrangements. If our drug candidates fail or do not gain regulatory approval, or if our drugs do not achieve market acceptance, we may not be profitable. As of December 31, 2010, we had an accumulated deficit of approximately $575.4 million. The extent of our future losses or profitability is highly uncertain.

Our ability to use net operating losses to offset future taxable income may be subject to certain limitations.

In general, under Section 382 of the Internal Revenue Code, a corporation that undergoes an "ownership change" is subject to limitations on its ability to utilize its pre-change net operating losses to offset future taxable income. Our existing net operating losses and credits may be subject to limitations arising from previous and future ownership changes under Section 382 of the Internal Revenue Code. To the extent we cannot completely utilize net operating loss carryforwards or tax credits in our financial statements to offset future taxable income, our tax expense may increase in future periods.

Because we expect to be dependent upon collaborative and license agreements, we might not meet our strategic objectives.

Our ability to generate revenue in the near term depends on the timing of recognition of certain upfront payments, achievement of certain milestone triggering events with our existing collaboration agreements and our ability to enter into additional collaborative agreements with third parties. Our ability to enter into new collaborations and the revenue, if any, that may be recognized under these collaborations is highly uncertain. If we are unable to enter into one or more new collaborations, our business prospects could be harmed, which could have an immediate adverse effect on our ability to continue to develop our compounds and on the trading price of our stock. Our ability to enter into a collaboration may be dependent on many factors, such as the results of our clinical trials, competitive factors and the fit of one of our programs with another company's risk tolerance, including toward regulatory issues, patent portfolio, clinical pipeline, the stage of the available data, particularly if it is early, overall corporate goals and financial position.